Filter Post Type

NewsVideoProductEventLink

Sort:

Most Recent

1–10 of 10

With the start of the new year, it is time to dust off the employee handbook, review your policies and procedures, and make sure they comply with all the new laws, regulations, and interpretations that have either already gone into effect or will in early 2023. Below, we have identified our “top 10” changes. Please keep in mind there were hundreds of laws, regulations, and changes implemented at the local, state, and federal levels throughout 2022. So, if you need a handbook/COVID-19 policy review or have any questions, please call. 1. California and Local Minimum Wage Raised – In addition to the gradual increase to minimum wage that has been in effect under California law, several Sonoma County cities have increased minimum wage beyond that required by the state. Below is a table that describes the state and local city requirements: Locality Effective Date Employers With 26 Or More Employees Employers With Less Than 26 Employees California 1/1/2023 $15.5

00

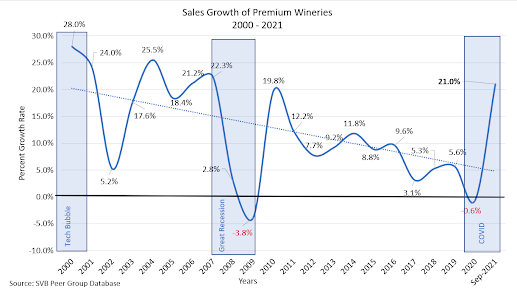

We all became unusually preoccupied in the U.S.starting somewhere around March 15th, 2020. I don't know about you, but the picture above was how I felt at that point in time. Since then, all of our thinking and behavior has evolved in a myriad of ways, and some of that evolution is permanent. I'm hopeful we are nearing the end of this queird social, economic, and health experiment. After getting sucked out of our realities by the COVID tornado, I think we are finally on the glide path that will land us in Oz. I know it won't be Kansas anymore when we lift from our comatose fog. It will be something different and probably in Technicolor. But whatever it is, it's going to be better than the last two years! Anyway, with all the distractions since 2020, I've been remiss in posting this blog. In my defense, I thought this post probably didn't matter given the other issues we were all facing. But the smoke is clearing, the vaccines and boosters are helping, Omi

00

February 5, 2021

Join Moss Adams and Bank of Marin as wine industry financial professionals discuss the issues and opportunities impacting the market. We’ll take questions from the audience and cover topics including: The current status and implications of Small Business Administration (SBA) Paycheck Protection Program (PPP) loans 2020 fires impact on the market Smoke taint-related tax credits and federal, state, and local tax considerations Free webinar: February 11, 2021 11:00 AM PST - 1 hour Register Here Speakers Marshall Graves, SVP, Sonoma County & Central Coast Commercial Banking Regional Manager, Bank of Marin Marshall is focused on growing the Bank’s customer base by building lasting banking relationships with local commercial and wine-related businesses. Leading an experienced lending team, he directs business development activities and oversees loan structuring and underwriting. Prior to this role, Marshall was a Senior Commercial Banking Manager and Wine Industry

00

January 27, 2021

The $900 billion COVID-19 relief bill, passed by Congress and signed into law on Dec. 27, includes a number of provisions that affect employers and their workers in terms of paid sick leave and Emergency Family and Medical Leave Act provisions. The legislation also boosts unemployment benefits to out-of-work Americans, as well as reopening and expanding the Paycheck Protection Program that was introduced in March as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Paid sick and family medical leave The new law did not extend the obligation for employers to provide emergency paid sick leave and expanded family and medical leave beyond Dec. 31, 2020, instead making it voluntary after that date. From Jan. 1, employers can continue receiving tax credits if they provide emergency paid sick leave (EPSL) and emergency family medical leave (EFML) to employees for COVID19-related purposes through March 31. Here are the caveats: Tax credits will be available for leave gran

00

This week the Senate returns from a two week, COVID-19 forced recess. The Senate Judiciary Committee has been in session working on the Supreme Court nomination hearings, but the full Senate has been out since the end of September. Senate Majority Leader McConnell (R-KY) has indicated that he intends to bring a smaller, $500 billion relief package up for a vote on the Senate floor. The package includes unemployment assistance, more money for schools and health care, and new funding for the Paycheck Protection Program for small businesses. The smaller measure will also contain liability protections so businesses, schools and health care providers that follow the appropriate health precautions can't be sued if people get sick. The bill is not expected to become law.

At the same time, Speaker Pelosi (D-CA) has continued negotiations with Treasury Secretary Mnuchin on a larger relief package. The President has expressed his willingness to sign another large relief package, but the ne

00

The terms of the usage of PPP loans were just substantially relaxed by the Paycheck Protection Program Flexibility Act of 2020 – H.R. 7010. PPP recipients now have 24 weeks (the “covered period”), to use the loan proceeds instead of the original eight weeks and still receive forgiveness of the loan amounts. However, recipients of already issued loans can elect to still use the original 8 week period for purposes of their forgiveness application calculations if that is more favorable.

The PPP Flexibility Act also provides significant relief involving the provisions that reduce loan forgiveness amounts where staffing levels have declined. It adds additional time to cure cuts in staffing or compensation levels that reduce forgiveness amounts, extending the deadline from June 30 to December 31, 2020. It also adds a provision that allows two exceptions to the forgiveness penalties for staffing reduction. Where the loan recipient can document that it was unable to rehire staff because t

00

April 27, 2020

On April 24, H.R. 266, the Paycheck Protection Program and Health Care Enhancement Act, was signed into law. In addition to providing significant funding for health care providers ($75 billion) and testing ($25 billion), the stimulus package revives the CARES Act’s Paycheck Protection Program (PPP) with an additional $310 billion in funding for forgivable loans. This expanded stimulus and relief package sets aside a portion of that funding for smaller lenders. The additional funding does not change the limits on the availability of the PPP’s forgivable loans, nor change the priority of borrowers in obtaining those loans.

However, in reaction to various reports on public companies obtaining PPP loans, the Treasury Department updated its PPP FAQs and this morning, April 24, issued additional proposed rules regarding the required certification that the “current economic uncertainty makes this loan request necessary,” and provided a safe harbor for entities that may have certified this

00

Last week Congress passed the Coronavirus Aid, Relief, and Economic Security Act, or the CARES Act, which was signed into law Friday, March 27, 2020. Among the extensive programs and economic incentives included in the legislation is the Paycheck Protection Program, which may benefit your business. The Paycheck Protection Program is an emergency loan program providing funding to cover your business’ payroll, debt service, utility, and rent costs incurred from February 15, 2020 through June 30, 2020 (the “covered period”). Eligibility While administered through the Small Business Administration, businesses eligible for the Paycheck Protection Program have been expanded to include any business concern with no more than 500 employees and includes, among others, sole proprietors, non-profits, independent contractors, and certain self-employed individuals. Full and part-time employees are counted toward the employee total. However, if your business is classified under NAIC

00

April 1, 2020

The U.S. Department of the Treasury announced today, March 31, that the SBA and the Treasury expect the CARES Act programs to be up and running by this Friday, April 3, 2020. You can find resources related to the CARES Act programs on Treasury’s website here, which is updated often and currently includes an application for borrowers for the Paycheck Protection Program (PPP). Additionally, the SBA has a resource page for small business that can be accessed here.

Significantly, the SBA is now indicating that 75% of PPP loan amounts will need to be spent on payroll as opposed to other allowed uses in order to qualify for loan forgiveness. It has also provided details on the loans, which will have relatively short, two year terms for the balance that is not forgiven, but with very low interest rates of 1%.

The Treasury and the IRS also have posted resources regarding the Employee Retention Tax Credit. But note that you cannot receive the payroll tax credit if you receive a PPP loan. A

00

What a week! Last week was really tough as we all struggled to navigate the quickly changing legal landscape, while working from home, often with kids in the background. We have heard from several HR Directors that it feels like they are trying to drink from a fire hose. We are hoping to help by providing a brief summary of what's been going on and how to find the critical information you need. FFCRA- Sick Leave: The Families First Coronavirus Response Act ("FFCRA") caused lots of headaches last week. Initially, it looked like all California non-essential employees still employed as of April 1, 2020, working for employers with fewer than 500 employees, would be eligible for two weeks of emergency paid sick leave ("EPSL"), because the order applied to all employees "subject to a federal, state, or local quarantine or isolation order related to COVID-19." As the Department of Labor ("DOL") issued further guidance on a daily basis, it becam

00